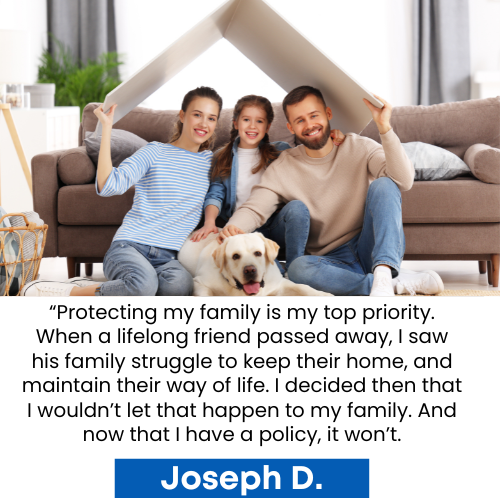

As a homeowner, being able to pay your mortgage on time every month is important. What would happen to your loved ones if you were to die prematurely, become disabled or critically ill, and your income suddenly disappeared? None of us know what the future will bring, but you can achieve peace of mind today with mortgage protection insurance.